The UNIQA Group and its subsidiaries are represented in 15 countries in Central and Eastern Europe. These companies operate around 1,500 service centres. In 2014, we generated more than 21 per cent of Group premiums in the CEE markets. We also work together with the subsidiaries of Raiffeisen Bank International AG in Eastern Europe as part of the preferred partnership that was renewed in 2013 for a period of 10 years.

Premium contribution of CEE to UNIQA Group

Area–wide //

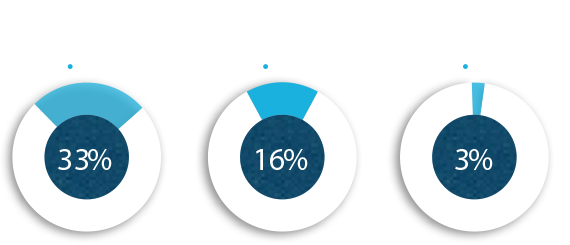

The UNIQA Group and its subsidiaries are represented in 15 countries in Central and Eastern Europe. In 2014, we generated more than 21 per cent of Group premiums in the CEE markets. The UNIQA Group is active in CEE in all types of insurance. Property and casualty insurance contributed a little over a third of the premiums, life insurance almost a fifth and health insurance 3 per cent.

Dense network in Central and Eastern Europe

We have a solid market position: our companies are among the top five insurers in nine CEE countries. In addition to exclusive sales, brokers and direct sales, we rely on the aforementioned cooperation with Raiffeisen Bank International AG. They have the largest banking network of a western bank in CEE. To strengthen our presence in Southeastern Europe, we acquired the insurance companies of the Baloise Group in Croatia and Serbia. The purchase was completed in March 2014.

We are pursuing a strong brand strategy in Central and Eastern Europe. In the spirit of our “one brand strategy”, we work in the CEE markets – with the exception of Russia – exclusively under the UNIQA brand name. In Russia, we rely exclusively on bank sales and operate under the “Raiffeisen Life” brand name.

Reaction to the current market trend

The trend in the CEE region was mediocre in 2014. Market growth remained below expectations in many countries. There were also the geopolitical tensions in Ukraine as well as the difficult market situation in Romania, in particular in the automobile insurance business.

We are responding to these challenges by focusing more closely on efficiency improvements and are also expanding our services for business customers: Since 2014, we have offered customised, cross-border insurance products aimed primarily at small to medium-sized enterprises in CEE.

Long-term growth outlook

Growth potential CEE

|

Good prospects // |

We remain convinced of the potential for growth in Central and Eastern Europe. With about 300 million inhabitants, the region offers an interesting future for insurers. It has a competitive export industry, flexible labour markets, investment-friendly tax and wage systems, low labour costs and well-educated employees. All of this enables economic growth that will outpace Western Europe in the long run.

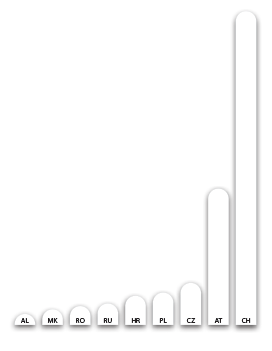

There is also the low insurance density: per capita expenditures for insurance products in CEE is significantly below comparable figures for Western Europe. While the average Austrian invests about €1,954 per year in his security, this figure is just €19 per capita in Albania. The figures per year for Ukraine are €53; for Hungary, €275; and for the Czech Republic, €503.

Growth rates in the CEE insurance markets are higher than those in markets that are already saturated. From UNIQA’s perspective, most of these markets still have room for expansion. The current economic outlook for 2015 may only allow us to expect moderate market development, but Central and Eastern Europe nevertheless remains the growth region for UNIQA – and the entire European continent.