With our long-term strategic programme UNIQA 2.0, we have defined a clear path to 2020: we are focusing on profitable growth in our core business as a primary insurer in our core markets of Austria and Eastern Europe.

Our business model – providing assurance

We, the UNIQA Group, are one of the leading providers of insurance in all categories in our core markets of Austria and Central and Eastern Europe (CEE). Our roots date back more than 200 years to 1811. Today, we look after more than nine million customers in 19 countries. The long-standing, successful cooperation with Austria’s largest banking group and one of the leading banks in CEE – Raiffeisen – is a key element of our business model. In addition to this, UNIQA is the strongest insurance brand in Austria and is very well positioned in CEE.

We provide assurance. In exchange for a premium, we take on our customers’ financial risk so they can be confident of being on firm ground. This gives them the assurance to shape their lives as they wish. In the event of a covered loss, we step in, compensate our customers and ensure that they are not left out of pocket. The basic principle of the insurance business is the pooling of risks. The premiums paid by all our policyholders form the basis for a “pot” of capital that we use to settle losses and claims as they arise. The value added we offer is the risk-adequate management of this portfolio and the optimal processing of claims. This means that we focus on risk diversification as well as a cost-effective corporate structure, thereby minimising risk and keeping our premiums attractive.

Proximity to our customers lies at the heart of our business model. We address people’s needs and inspire them with innovative solutions in the areas of property and casualty, life, and health insurance, while never losing sight of the profitability of our products.

Our strategy – profitable growth

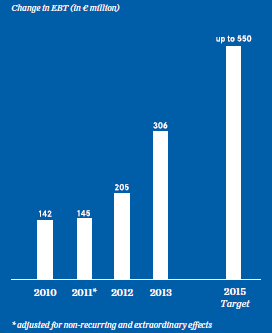

Earnings growth due to UNIQA 2.0 |

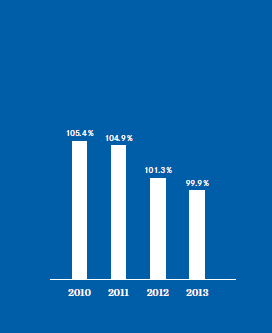

Combined ratio reduced |

Combined RatioThe ratio of insurance benefits and costs to premiums in property and casualty insurance is described as the combined ratio. This figure illustrates the ability of a property insurance company to generate a profit from its core operating business. In 2013, UNIQA succeeded in reducing its combined ratio to 99.9 per cent, thereby making a significant contribution to improving the profitability of its core business. |

For us, the UNIQA 2.0 strategic programme represents a commitment to our shareholders, customers and employees. We are working to become the best insurance company in Central Europe. This means we want to be the insurance company with the strongest focus on the needs of shareholders, customers and employees.

In 2013, we achieved what we promised. We increased our customer base to 9.3 million. Earnings before taxes (EBT) increased by 49.7 per cent year-on-year to € 306 million, while consolidated profit after taxes and minority interests more than doubled. This also enables us to propose an increase in the dividend from €0.25 to €0.35 per share.

The low interest rate environment remains a particular challenge for the entire European insurance industry at present. This is making us work all the harder to improve our underwriting result, i.e. improving the profitability of our core business. The Group-wide combined ratio has fallen to 99.9 per cent, while our cost ratio has been reduced to 24.1 per cent. The capital increase (re-IPO) that was successfully implemented in October 2013 also strengthened our equity base and created strategic flexibility for further growth. We already fulfil the new capitalisation requirements for insurance companies (Solvency II) that will come into force within the EU on 1 January 2016.