The focus of risk management with management structures and defined processes is the attainment of UNIQA’s and its subsidiaries’ strategic goals.

UNIQA’s Risk Management Guidelines form the basis for a uniform standard at various company levels. The guidelines are approved by the Group CRO and the full Management Board and describe the minimum requirements in terms of organisational structure and process structure. They also provide a framework for all risk management processes for the most important risk categories.

In addition to the Group Risk Management Guidelines, similar guidelines have also been prepared and approved for the Company’s subsidiaries. The Risk Management Guidelines at subsidiary level were approved by the Management Board of the UNIQA subsidiaries and are consistent with UNIQA’s Risk Management Guidelines.

They aim to ensure that risks relevant to UNIQA are identified in advance and evaluated. If necessary, proactive measures are introduced to transfer or minimise the risk.

Intensive training on the content and utilisation of these guidelines is required in order to ensure that risk management is incorporated in everyday business activities. Extensive informative and training measures have therefore been taken since 2012; they will be continued in the future and extended to additional target groups.

7.2.1 Organisational structure (governance)

The detailed set-up of the process and organisational structure of risk management is set out in UNIQA’s Risk Management Guidelines. They reflect the principles embodied in the concept of “three lines of defence” and the clear differences between the individual lines of defence.

First line of defence: risk management within the business activity

Those responsible for business activities must develop and put into practice an appropriate risk control environment to identify and monitor the risks that arise in connection with the business and processes.

Second line of defence: supervisory functions including risk management functions

The risk management function and the supervisory functions, such as controlling, must monitor business activities without encroaching on operational activities.

Third line of defence: internal and external auditing

This enables an independent review of the formation and effectiveness of the entire internal control system, which comprises risk management and compliance (e.g. internal auditing).

")

1) Beginning 1 January 2015 in an interlocking directorate together with the CFO

Management Board and Group functions

The UNIQA Insurance Group AG Management Board is responsible for establishing the business policy objectives and determining the associated risk strategy. The core components of the risk management system and the associated governance are enshrined within the UNIQA Group Risk Management Policy adopted by the Management Board.

The function of Chief Risk Officer (CRO)[1] is a separate area of responsibility at the Group Management Board level. This ensures that risk management is represented on the Management Board. The CRO is supported in the implementation and fulfilment of risk management duties by the Group Actuarial and Risk Management unit. A central component of the risk management organisation is UNIQA’s risk management committee, which carries out monitoring and initiates appropriate action in relation to the current development and the short and long-term management of the risk profile. The risk management committee establishes the risk strategy, monitors and controls compliance with risk-bearing capacity and limits, and therefore plays a central role in the management process implemented under UNIQA’s risk management system.

Operative insurance companies

In the operative insurance companies, the CRO function has also been established at Management Board level, with the functions of the risk manager at the next level down. A consistent, uniform risk management system has therefore been set up throughout the Group.

As at Group level, each of the operative insurance companies has its own risk management committee, which forms a central element of the risk management organisation. This committee is responsible for the management of the risk profile and the associated specification and monitoring of risk-bearing capacity and limits.

The Supervisory Board at UNIQA Insurance Group AG receives comprehensive risk reports at Supervisory Board meetings.

7.2.2 Risk management process

UNIQA’s risk management process delivers periodic information about the risk profile and enables the top management to make the decisions for the long-term achievement of objectives.

The process concentrates on risks relevant to the Company and is defined for the following risk categories:

- Actuarial risk (property and casualty insurance, health and life insurance)

- Market risk/Asset-Liability Management risk (ALM risk)

- Credit risk/default risk

- Liquidity risk

- Concentration risk

- Strategic risk

- Reputational risk

- Operational risk

- Contagion risk

A Group-wide, standardised risk management process regularly identifies, evaluates and reports on risks to UNIQA and its subsidiaries within these risk categories.

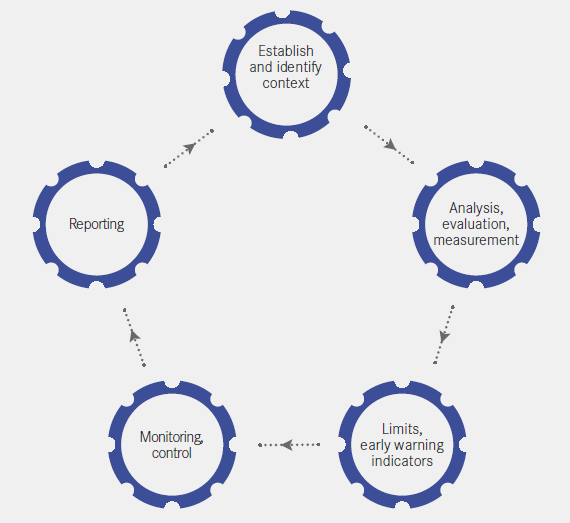

UNIQA’s risk management process

Risk identification:

Risk identification is the starting point for the risk management process, systematically recording all major risks and describing them in as much detail as possible. In order to conduct as complete a risk identification as possible, different approaches are used in parallel, and all risk categories, subsidiaries, processes and systems are included.

Evaluation/measurement:

The risk categories of market risk, technical risk, counterparty default risk and concentration risk are evaluated at UNIQA by means of a quantitative method based on the standard approach of Solvency II and the ECM approach. Furthermore, risk drivers are identified for the results from the standard approach and analysed to assess whether the risk situation is adequately represented (in accordance with the Company’s Own Risk and Solvency Assessment (ORSA)). All other risk categories are evaluated quantitatively or qualitatively with their own risk scenarios.

The scenario analysis (of UNIQA’s economic, internal and external risk situation) is generally a crucial element in the risk management process.

A scenario is a possible internal or external event that has a short-term or medium-term effect on consolidated profit or loss, the solvency position or sustainability of future results. The scenario is formulated with respect to its inherent characteristic (e.g. the start of Greece’s insolvency) and evaluated in terms of its financial effect on UNIQA. The likelihood that the scenario will actually occur is also considered.

Limits/early warning indicators:

The limit and early warning system determines risk-bearing capacity (available equity according to IFRS, financial equity) and capital requirements on the basis of the risk situation at ongoing intervals, thereby deriving the level of coverage. If critical coverage thresholds are reached, then a precisely defined process is set in motion, the aim of which is to bring the level of solvency coverage back to a non-critical level.

Reporting:

A quarterly report on the solvency situation along with a monthly risk report on the biggest risks identified are prepared for each operational company and for the UNIQA Group on the basis of detailed risk analysis and monitoring. The reports for each individual UNIQA subsidiary and the UNIQA Group itself have the same structure, providing an overview of major risk indicators such as risk-bearing capacity, solvency requirements and risk profile. In addition, quantitative and qualitative reporting (in the form of the quantitative reporting templates and the narrative report respectively) is implemented for the UNIQA Group and for all subsidiaries for which Solvency II reporting is mandatory.

7.2.3 Activities and objectives in 2015

Based on external and internal developments, activities in 2015 focused on the following:

- Preparation work for the implementation of Solvency II

- Reduction in the risks caused by the period of low interest rates

Preparation work for the implementation of Solvency II

Solvency II is an EU-wide project, the objective of which is to achieve a fundamental reform of solvency regulations (capital requirements) for insurance companies. The existing static system for determining capital requirements is to be superseded by a risk-based system. One of the main changes in the new system is that it is to take greater account of qualitative elements such as internal risk management.

Following publication of the preparation guidelines by the European Insurance and Occupational Pensions Authority (EIOPA) in October 2013 and the implementation of these guidelines in the Austrian Insurance Supervision Act (VAG) of June 2014, it is now clear what preparation work is needed before Solvency II comes into force on 1 January 2016.

As in previous years, in 2015 specific preparatory steps were again taken based on this information, both in the UNIQA Group and in the operating units. This included in particular

- Development of quantitative reports (QRTs)

- Development of narrative reports

- Preparatory work for future reporting in general (SFCR, RSR, AFR)

- Further development of the Company’s Own Risk and Solvency Assessment (ORSA)

- Further development of the partial internal model for the property/casualty insurance business.

- Further development of comprehensive limits

- Increase in the frequency of solvency calculations

In addition, a comprehensive training programme for senior managers, other managers, and employees in key functions is a core component of a fully functioning Group-wide risk management framework. Understanding of the objectives and the impact of the risk management approach in the context of value-based management should be achieved. A great deal of importance is also attached to training the Supervisory Board of the UNIQA Insurance Group AG so that the members of the Supervisory Board are well informed about the ongoing developments in the management approach (economic management) and can take these developments into account with respect to their supervisory activities.

In both cases, the discussion about the use of the information from the risk capital models, in particular from the partial internal model relating to property/casualty insurance, is a relevant point, allowing users to make the connection between this information and the ongoing business.

Reduction in the risks caused by the period of low interest rates

The interest rate environment that remained low and volatile in 2015 meant that a restrictive approach was still required in terms of new products and asset liability management, particularly in life insurance.

Group guidelines ensure that products are subject to a standardised profitability test before being launched on the market and achieve minimum defined margins in terms of their expected value. The guaranteed discount rate for new traditional life insurance products was reduced even further in many UNIQA companies as a result of the interest rates, often below the relevant maximum rate permissible by statute.

The domestic market of Austria which continues to be characterised by strong customer demand for life insurance products should be mentioned as a particular example of this. Here, at UNIQA Austria and Raiffeisen Versicherung AG, the products in the traditional life insurance line were completely revised as of 1 January 2015 and given the title “New Classic” (“Klassik Neu”). The “New Classic” will give customers a 100 per cent capital guarantee on net premiums, high repurchase values from the beginning, along with the possibility of making variable additional payments and withdrawals during the term. In addition, costs and fees are spread out proportionally over the entire term and no longer taken from the premium but rather from the profit. The entire premium amount (excl. insurance tax) thus flows directly into the investment, resulting in a considerably higher savings premium from the beginning than is offered by conventional life insurance. This means the product offers customers much more transparency and flexibility.

From the Company’s point of view, this product concept has the advantage that, among other things, the discount rate is set at 0 per cent, which leads, in particular on longer terms, to a reduction of the guarantee requirement. In addition, this new product concept also meets the future legal requirements concerning transparency and capital adequacy. The year 2015 was an impressive example of how the route followed meets both customer needs and earnings requirements, even though product developments are being introduced on a continuous basis. In Austria, for instance, more than 40.000 policies of the “New Classic” product were sold in 2015, which exceeded our expectations.

In Asset Liability Management (ALM), the process was consistently continued to reduce the duration gap even further, which involves more effectively adjusting the terms of the assets to the terms of the liabilities. The option of running a regular/year-round procedure to draw up the risk profile and associated limits represents a key element of the ALM process in UNIQA. Management is carried out on the basis of risk capital consumption and associated limits, which enables the Group to make strategic decisions on the basis of a value-based risk/return analysis.

In 2015, the Group focused not only on the necessary standard processes but also on scenario analyses, especially the possible changes in the liabilities profile depending on different interest rate situations. In this case, the analysis of the life insurance business plays a central role because it is difficult to predict a change in the lapse or surrender pattern for customer policies in response to a specific trend in interest rates. Associated risks were analysed and action implemented to cushion these risks.